Do Capital Gains Tax Cuts Increase Revenue?

At the end of my November 8th post, I asked for anyone who knows of an economic study that purports to show that any income tax cut has paid for itself to please post a link to it. On November 18th, I received the following reply:

I'm not an economist of any flavor, but I was wondering what you thought of the article by Stephen J Entin from the Institute for Research on the Economics of Taxation that I've linked below. He appears to argue that increased capital gains tax should decrease net federal revenues.

Any thoughts appreciated.

http://iret.org/pub/CapitalGains-1.pdf

The rest of this post will attempt to answer this reply:

My request at the end of my November 8th post did refer to income tax cuts, not capital gains tax cuts and those are the primary focus of my analysis which I referenced there. The only involved analysis of capital gains tax cuts that I have done are in my prior posts, here, here, and here. Following is my chief conclusion from that relatively short analysis:

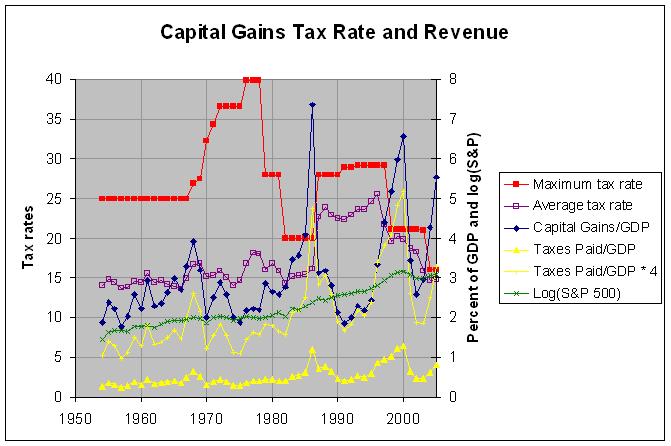

The above discussion points to how difficult it is to study the relationship between capital gains tax rates and revenues. Hence, it is not intended to show a simple relationship but rather to show the problems with claims of simple relationships derived from looking at a few changes in the capital gains tax rate. That said, I did notice one interesting relationship in the data. From 1954 to 1982, there appeared to have been something of a positive correlation between the average capital gains tax rate and capital gains revenue. That is, they both tended in increase or decrease at the same time. After 1982, there appeared to be much more volatility in both the average tax rate and revenue and any obvious positive correlation disappeared. This would suggest that a more stable average tax rate might be desirable. This would lessen the need for investors to concern themselves with the timing of their stock transactions and allow them to concern themselves only with the long-term value of the investments themselves. If at any point that it is decided that the tax rate needs to be changed, it would likely be wise to phase in the change slowly.

Following is a graph of the data that this paragraph is referring to:

I did take a quick look through the paper you referenced and do have a few thoughts. First of all, I had some comments on the second paragraph which reads as follows:

However, taxpayers react to higher tax rates by earning and reporting less income. Higher taxes on capital retard capital formation and reduce wages across the board. The particular tax increases that the Congress and the Administration are most likely to adopt would damage the economy and reduce the tax base. In fact, they are likely to result in lower federal revenues, and larger budget deficits.

Except for the word "likely", these statements seems a bit absolute. In any event, this proposed effect is possibly countered by other effects. Consider the following excerpt from an article titled "Policy Points: Experts Agree That Capital Gains Tax Cuts Lose Revenue":

To raise revenue over the long run, capital gains tax cuts would need to have extraordinary huge, positive effects on saving, investment, and economic growth that virtually no respected expert or institution believes they have. In fact, experts are not even sure that the long-term economic effects of these capital gains tax cuts are positive rather then negative.

One reason is that preferential tax rates for capital gains encourage tax sheltering, by creating incentives for taxpayers to take often-convoluted steps to reclassify ordinary income as capital gains. This is economically unproductive and wastes resources. The Urban-Brookings Tax Policy Center’s director Leonard Burman, one of the nation’s leading tax experts, has explained, “shelter investments are invariably lousy, unproductive ventures that would never exist but for tax benefits.” Burman has concluded that, “capital gains tax cuts are as likely to depress the economy as to stimulate it.”

Secondly, I did notice that the paper seems to concede that it is in disagreement with the Treasury and Joint Tax Committee of the Congress. On page 3, it states:

The Office of Tax Analysis at the Treasury and the staff of the Joint Tax Committee of the Congress estimate revenues for the Federal budget. They also estimate changes in revenue associated with proposed changes in tax policy. They base their revenue forecasts on an assumed underlying state of the economy (the baseline economic forecast). The economic baseline specifies the amounts of total output, employment, capital, and the various types of income associated with them (the macro-economic conditions).

The revenue estimates of a proposed tax change are conducted on the assumption that the macro-economic baseline, with its aggregate levels of income and output, labor and capital, is fundamentally unchanged. This is called static revenue estimation. By contrast, estimation that allows for tax changes or other budget changes to affect macro-economic conditions, such as the size of the economy and the level of income, is called dynamic revenue estimation.

This disagreement is also mentioned by the CBPP article which also mentions the non-partisan Congressional Budget Office (CBO) and the Administration’s Office of Management and Budget as estimating that cutting capital gains rates reduces revenues over the long run. The paper does suggest in the excerpt above that this disagreement is because it is using a presumedly better dynamic revenue estimation versus static revenue estimation being used by the other studies. However, the CBO did do at least one study using various supply-side models in 2004 to analyze President Bush's proposals which included extending the tax cuts. As can be seen in the summary of that study at this link, those models estimated a significant cost just as did the conventional model. Now those proposals did include more than a capital gains tax cut. Still, it does show a case where the use of dynamic models by the CBO has had no significant effect on the estimated costs.

Thirdly, the conclusions of the paper seem to be based strictly on a theoretical model, the Cobb Douglas production function described starting on page 36. Although this model was doubtlessly analyzed against real data, the paper does not appear to do any analysis of recent data. Hence, I could only search for critiques of this model. This link states that the "Cobb-Douglas production function was largely abandoned after 1961" and there are some criticisms listed in the

Wikipedia entry for the model. It's not an easy thing to judge these criticisms but neither is it easy to judge the Cobb-Douglas production function itself.

In any event, the paper does seem to agree that there is a significant difference between the effect of income tax cuts and capital gains tax cuts. The following excerpt is from page 22:

The supply of labor is rather inelastic. Many primary workers (the main breadwinners in the households) are employed by others, and have limited ability to vary their hours worked (set by their employers) or the degree to which they participate in the work force (each family needs at least one breadwinner). Their hours worked do not vary a lot as wages rise or fall (so the supply curve in Chart 1 is steeply vertical.) Such workers are assumed to bear most of any taxes imposed on labor, including the income tax and the payroll tax, both the employee and employer shares. Secondary workers in the family, the self-employed, teenagers, and wealthier individuals have somewhat more flexibility in deciding whether or not to work, and how many hours to offer, but even they bear most of the tax on their labor income.

The effect of taxes on capital is quite different. The quantity of capital is far more sensitive to taxes than is the quantity of labor. (Its supply curve is more nearly horizontal.) It is easy and enjoyable to consume instead of save, and quite possible to invest abroad instead of in one’s own country. If the after-tax rate of return on saving and investment in the United States is driven down by an increase in the tax rate, U.S. capital formation may be curtailed, or shifted to other countries. The same phenomenon occurs within the country. When there is a tax increase on capital in any one jurisdiction, the amount of plant, equipment, and buildings in that region shrinks. As the capital becomes scarce, the rate of return on the remaining capital rises, until it is again earning a normal rate of return, after tax.

So this paper does not seem to be in any way suggesting that income tax cuts pay for themselves. Hence, I am still yet to find a single economic study that purports to show evidence that any income tax cut has ever paid for itself and would be interested in any that someone could post a link to. However, I am also interested in any additional studies that make that claim about capital gains tax cuts. Anyhow, I hope these thoughts were helpful to the commenter who asked for them. Feel free to leave any additional comments or questions.

I'm not an economist of any flavor, but I was wondering what you thought of the article by Stephen J Entin from the Institute for Research on the Economics of Taxation that I've linked below. He appears to argue that increased capital gains tax should decrease net federal revenues.

Any thoughts appreciated.

http://iret.org/pub/CapitalGains-1.pdf

The rest of this post will attempt to answer this reply:

My request at the end of my November 8th post did refer to income tax cuts, not capital gains tax cuts and those are the primary focus of my analysis which I referenced there. The only involved analysis of capital gains tax cuts that I have done are in my prior posts, here, here, and here. Following is my chief conclusion from that relatively short analysis:

The above discussion points to how difficult it is to study the relationship between capital gains tax rates and revenues. Hence, it is not intended to show a simple relationship but rather to show the problems with claims of simple relationships derived from looking at a few changes in the capital gains tax rate. That said, I did notice one interesting relationship in the data. From 1954 to 1982, there appeared to have been something of a positive correlation between the average capital gains tax rate and capital gains revenue. That is, they both tended in increase or decrease at the same time. After 1982, there appeared to be much more volatility in both the average tax rate and revenue and any obvious positive correlation disappeared. This would suggest that a more stable average tax rate might be desirable. This would lessen the need for investors to concern themselves with the timing of their stock transactions and allow them to concern themselves only with the long-term value of the investments themselves. If at any point that it is decided that the tax rate needs to be changed, it would likely be wise to phase in the change slowly.

Following is a graph of the data that this paragraph is referring to:

I did take a quick look through the paper you referenced and do have a few thoughts. First of all, I had some comments on the second paragraph which reads as follows:

However, taxpayers react to higher tax rates by earning and reporting less income. Higher taxes on capital retard capital formation and reduce wages across the board. The particular tax increases that the Congress and the Administration are most likely to adopt would damage the economy and reduce the tax base. In fact, they are likely to result in lower federal revenues, and larger budget deficits.

Except for the word "likely", these statements seems a bit absolute. In any event, this proposed effect is possibly countered by other effects. Consider the following excerpt from an article titled "Policy Points: Experts Agree That Capital Gains Tax Cuts Lose Revenue":

To raise revenue over the long run, capital gains tax cuts would need to have extraordinary huge, positive effects on saving, investment, and economic growth that virtually no respected expert or institution believes they have. In fact, experts are not even sure that the long-term economic effects of these capital gains tax cuts are positive rather then negative.

One reason is that preferential tax rates for capital gains encourage tax sheltering, by creating incentives for taxpayers to take often-convoluted steps to reclassify ordinary income as capital gains. This is economically unproductive and wastes resources. The Urban-Brookings Tax Policy Center’s director Leonard Burman, one of the nation’s leading tax experts, has explained, “shelter investments are invariably lousy, unproductive ventures that would never exist but for tax benefits.” Burman has concluded that, “capital gains tax cuts are as likely to depress the economy as to stimulate it.”

Secondly, I did notice that the paper seems to concede that it is in disagreement with the Treasury and Joint Tax Committee of the Congress. On page 3, it states:

The Office of Tax Analysis at the Treasury and the staff of the Joint Tax Committee of the Congress estimate revenues for the Federal budget. They also estimate changes in revenue associated with proposed changes in tax policy. They base their revenue forecasts on an assumed underlying state of the economy (the baseline economic forecast). The economic baseline specifies the amounts of total output, employment, capital, and the various types of income associated with them (the macro-economic conditions).

The revenue estimates of a proposed tax change are conducted on the assumption that the macro-economic baseline, with its aggregate levels of income and output, labor and capital, is fundamentally unchanged. This is called static revenue estimation. By contrast, estimation that allows for tax changes or other budget changes to affect macro-economic conditions, such as the size of the economy and the level of income, is called dynamic revenue estimation.

This disagreement is also mentioned by the CBPP article which also mentions the non-partisan Congressional Budget Office (CBO) and the Administration’s Office of Management and Budget as estimating that cutting capital gains rates reduces revenues over the long run. The paper does suggest in the excerpt above that this disagreement is because it is using a presumedly better dynamic revenue estimation versus static revenue estimation being used by the other studies. However, the CBO did do at least one study using various supply-side models in 2004 to analyze President Bush's proposals which included extending the tax cuts. As can be seen in the summary of that study at this link, those models estimated a significant cost just as did the conventional model. Now those proposals did include more than a capital gains tax cut. Still, it does show a case where the use of dynamic models by the CBO has had no significant effect on the estimated costs.

Thirdly, the conclusions of the paper seem to be based strictly on a theoretical model, the Cobb Douglas production function described starting on page 36. Although this model was doubtlessly analyzed against real data, the paper does not appear to do any analysis of recent data. Hence, I could only search for critiques of this model. This link states that the "Cobb-Douglas production function was largely abandoned after 1961" and there are some criticisms listed in the

Wikipedia entry for the model. It's not an easy thing to judge these criticisms but neither is it easy to judge the Cobb-Douglas production function itself.

In any event, the paper does seem to agree that there is a significant difference between the effect of income tax cuts and capital gains tax cuts. The following excerpt is from page 22:

The supply of labor is rather inelastic. Many primary workers (the main breadwinners in the households) are employed by others, and have limited ability to vary their hours worked (set by their employers) or the degree to which they participate in the work force (each family needs at least one breadwinner). Their hours worked do not vary a lot as wages rise or fall (so the supply curve in Chart 1 is steeply vertical.) Such workers are assumed to bear most of any taxes imposed on labor, including the income tax and the payroll tax, both the employee and employer shares. Secondary workers in the family, the self-employed, teenagers, and wealthier individuals have somewhat more flexibility in deciding whether or not to work, and how many hours to offer, but even they bear most of the tax on their labor income.

The effect of taxes on capital is quite different. The quantity of capital is far more sensitive to taxes than is the quantity of labor. (Its supply curve is more nearly horizontal.) It is easy and enjoyable to consume instead of save, and quite possible to invest abroad instead of in one’s own country. If the after-tax rate of return on saving and investment in the United States is driven down by an increase in the tax rate, U.S. capital formation may be curtailed, or shifted to other countries. The same phenomenon occurs within the country. When there is a tax increase on capital in any one jurisdiction, the amount of plant, equipment, and buildings in that region shrinks. As the capital becomes scarce, the rate of return on the remaining capital rises, until it is again earning a normal rate of return, after tax.

So this paper does not seem to be in any way suggesting that income tax cuts pay for themselves. Hence, I am still yet to find a single economic study that purports to show evidence that any income tax cut has ever paid for itself and would be interested in any that someone could post a link to. However, I am also interested in any additional studies that make that claim about capital gains tax cuts. Anyhow, I hope these thoughts were helpful to the commenter who asked for them. Feel free to leave any additional comments or questions.

Reed, I see that I am the only one to have dug deeply enough to find your excellent commentary on this issue. Thanks for making the effort.

ReplyDeleteAlan Hamerstrom

The issue is the elasticity of taxable income or, in the case of capital gains, the elasticity of realizations (if the tax rate rises, there is less trading). In the case of overall taxable income several studies estimate that it may be close to unity (1) for those in the top 1 percent. If so, a higher tax rate would not yield revenue and a lower rate would not lose revenue. When it comes to capital gains, more than a dozen studies find Entin's conclusion correct. I survey some of this literature in a recent paper: http://www.cato.org/speeches/reynolds_FMF092608.pdf

ReplyDelete