The Problems with "Taxpayer Examples"

Today, House Speaker Paul Ryan (R-WI), Ways and Means Committee Chairman Kevin Brady (R-TX), and other members of House leadership and the Ways and Means Committee introduced the Tax Cuts and Jobs Act—bold legislation to overhaul America’s tax code for the first time in 31 years. With this bill, a typical middle-income family of four, earning $59,000 (the median household income), will receive a $1,182 tax cut.

At the end of the release is a link to descriptions of this and several other examples of how the proposed tax cuts would save money for various types of taxpayers. I've created an R Shiny application which can interactively show the tax savings for the first four examples and other variations. That application can be accessed at this link.

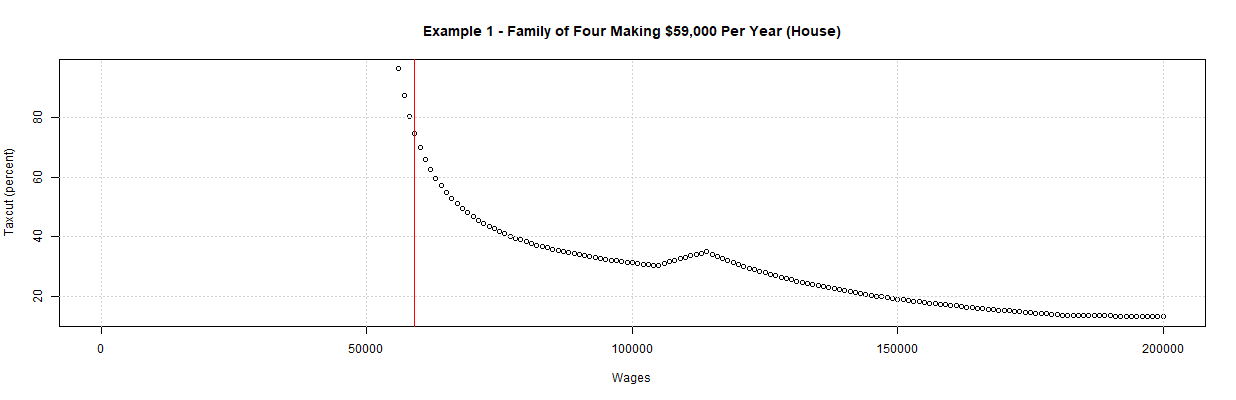

Selecting "Example 1" in the "Tax Examples" select list causes the following table and plot to be output:

Names Taxes Released

1 Current 2017 1582.50000 1582

2 House Bill 400.00000 400

3 Change -1182.50000 -1182

4 % Change -74.72354

The second column shows the calculated taxes and the third column shows the taxes reported in the press release. As can be seen in the table, they are almost identical. The plot, on the other hand, shows the percent taxcut for the example but does so for all incomes from $0 to $200,000 with the example's income denoted by a red vertical line. As can be seen, this income has one of the higher tax cuts among those displayed.

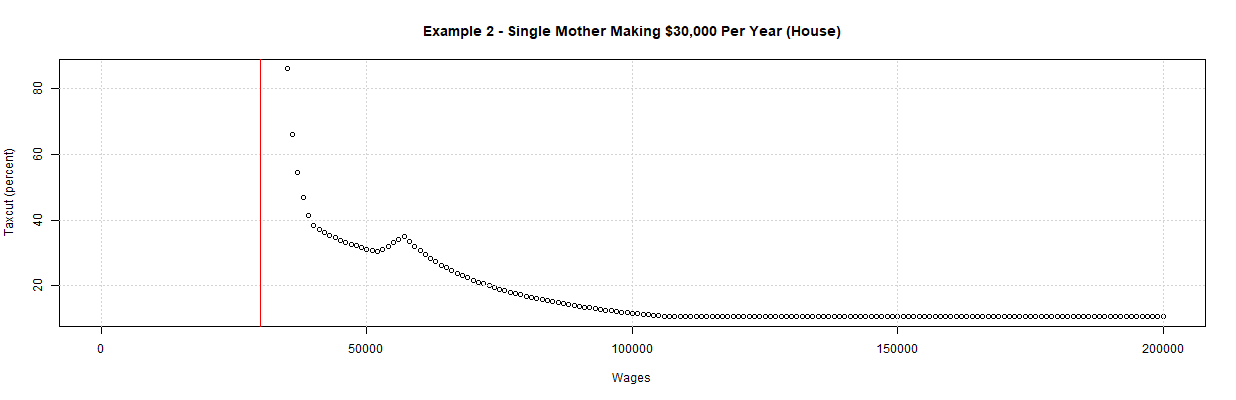

Selecting "Example 2" in the "Tax Examples" select list causes the following table and plot to be output:

Names Taxes Released

1 Current 2017 -670.54660

2 House Bill -1276.79660 < -1000

3 Change -606.25000 < -700

4 % Change 90.41132

Note: Taxes for both plans include an EITC of $1536.7966 (using the 2017 formula)

As can be seen in the third column of the table, the press release was somewhat vague about the tax numbers for this example, stating that "Cindy will receive a tax refund of over $1,000" which is "over $700 larger than the refund she receives today. However, the second column shows her paying taxes in both cases, not getting a refund. The $1277 tax refund for the House Bill can be verified by the following calculation:

($30,000 - $12,000) * 0.12 - $1600 - $300 - $1537 = -$1277In this calculation, $12,000 is the standard deduction for single taxpayers, 0.12 is the 12% tax rate, $1,600 is the child credit for the child, and $300 is the family credit for the mother. Finally, the $1537 is the Earned Income Tax Credit (EITC) as calculated using the 2017 formula.

Hence, the figure for the House Bill refund is "over $1,000" but it is just $606 more than the current refund, not "over $700 larger than the refund she receives today". To my knowledge, the House Bill has not changed how EITC is calculated and is using the 2017 formula. In any case, $606 rather than "over $700" is a relatively small disagreement.

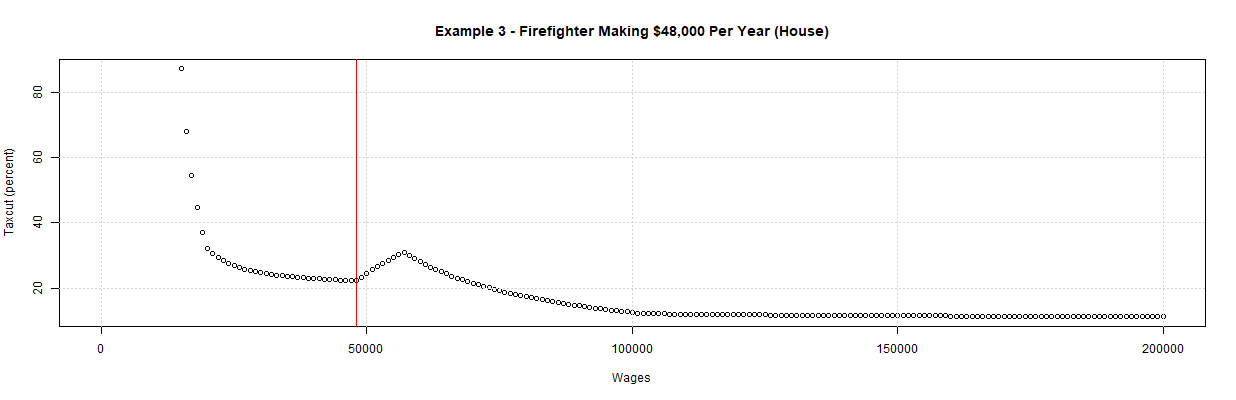

Selecting "Example 3" in the "Tax Examples" select list causes the following table and plot to be output:

Names Taxes Released

1 Current 2017 5173.75000 5173

2 House Bill 4020.00000 3872

3 Change -1153.75000 -1301

4 % Change -22.30007

As can be seen from the table, the numbers for the Current 2017 taxes do match but the calculation for the House Bill taxes is $148 greater than the releases figure. The $4,020 figure can be verified by the following calculation:

($48,000 - $12,000) * 0.12 - $300 = $4,020.Hence, the $3,872 figure appears to be in error. Unlike the prior two examples, however, the plot shows that the income of $48,000 provides among the lower tax cuts for incomes under about $60,000.

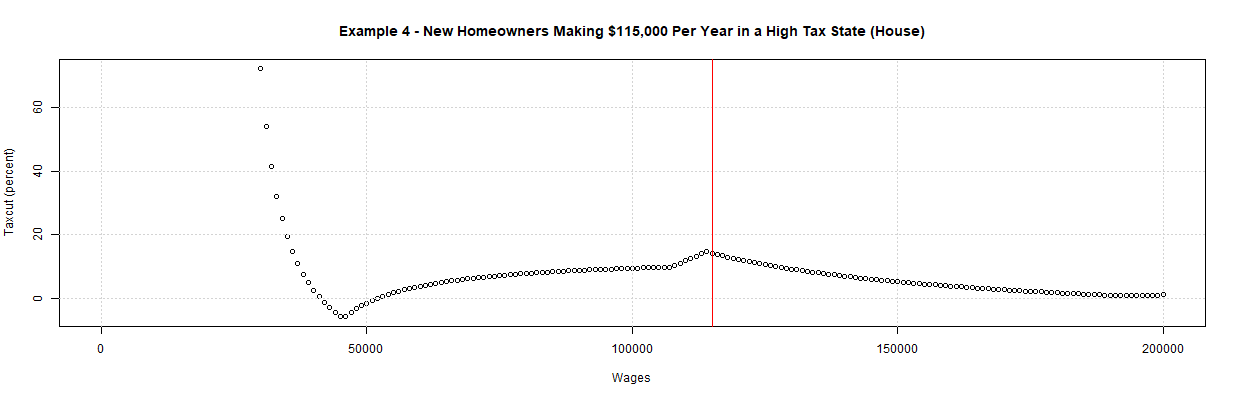

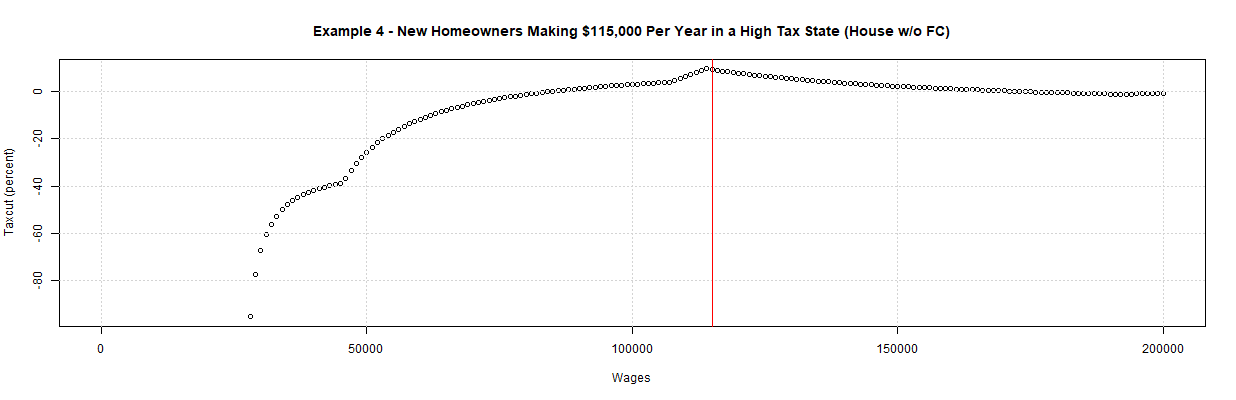

Finally, selecting "Example 4" in the "Tax Examples" select list causes the following table and plot to be output:

Names Taxes Released

1 Current 2017 12180.00238 12180

2 House Bill 10450.00000 11050

3 Change -1730.00238 -1130

4 % Change -14.20363

The press release specifies that the taxpayers in this example "will pay $8,400 in mortgage interest and $6,900 in state and local property taxes". However, it does not specify how much they paid in state and local taxes despite stating that they were in a "high tax state". For this reason, I calculated that paying 7.64347 percent of their income in state and local taxes would have provided them with the deduction to achieve the $12,180 figure for Current 2017 taxes given in the press release. With no deduction for state and local taxes, their taxes would have been $14,377.50.

As can be seen from the table, the calculated taxes for the House Bill is $10,450, exactly $600 less than the $11,050 figure given in the press release. This suggests that the figure in the press release may have been calculated without including the family credit of $300 per person. This can be checked by selecting "House Bill w/o Family Credits" in the "Tax Plan 2" select list. In that case, the following table and plot are output:

Names Taxes Released

1 Current 2017 12180.002375 12180

2 House Bill w/o Family Credits 11050.000000 11050

3 Change -1130.002375 -1130

4 % Change -9.277522

Now, the calculated taxes match those in the press release. Also, the plot shows that the income of $115,000 has about the highest tax cut among those displayed.

The selection of "House Bill w/o Family Credits" is appropriate for another reason. A Washington Post article points out that the "new Family Flexibility Credit of $300 for each tax filer and another $300 for a spouse" expires after five years. It links to an analysis by David Kamin, a tax law professor at New York University which goes into more details. It shows that, because of this and other provisions in the House Bill tax bill, the tax cut shown in the first example would turn into a tax hike over current law in 2024 and beyond.

The above two plots show something else that's interesting. In the fourth example, the House Bill represent a tax hike for some lower income taxpayers in the first year. For example, selecting "Example 4" and changing "Wages, salaries, tips, etc." to 45000 causes the following table to be output:

Names Taxes Released

1 Current 2017 1816.043850 12180

2 House Bill 1920.000000 11050

3 Change 103.956150 -1130

4 % Change 5.724319

Hence, the House Bill represent a 5.7 percent tax increase in this case. Of course, the 7.64347 percent of income for state and local taxes may be a bit high for this income level. Still, you can move this number to "Medical and dental expenses (% over 10% of income)" and set state and local taxes to 0 and get the same result. Or, alternately, you can set both medical and state & local taxes to zero, set "Charitable contributions" to $3,440 and get about the same result.

The biggest concern raised by the House Bill bill is likely the higher taxes that they represent to some lower income taxpayers in the first year and to many more lower income taxpayers in future years. Also, the above plots show that it is helpful to look at taxpayer examples over broad ranges of income. Still, it is very concerning that the examples released by the office of Speaker Paul Ryan (which came from the Committee of Ways and Means) appear to contain a number of errors. This suggests that, even for something as seemingly simple as the calculation of taxes under various plans, publications should show their work.

The Problems with "Taxpayer Examples" (Part 2)

Who Will See Their Taxes Go Up under the House and Senate Plans?

Comments

Post a Comment